84–85 Bankstown City Plaza

Report menu jump to sections

Executive Summary

The site has a clear, evidence-backed story: a flexible ground-floor tenancy in a pedestrian and transport-led Bankstown CBD precinct.

This report is intended to make that story easier to communicate to prospective tenants and decision-makers. It combines location context, observed customer behaviour, reachable market depth and tenant-fit signals into a practical view of the opportunity.

The data points to four useful conclusions:

- The setting is a strength: metres from Bankstown Station, moments from Bankstown Central, and positioned within an established plaza / food / service precinct.

- The market behind the site is meaningful: the 5-minute drive market has around 61,000 residents and approximately $1.8B in annual retail spend within a five-minute drive time.

- The observed behaviour is strong: the site records approximately 1.46M annual visits, and the customers observed around the site represent approximately $5.5B of annual spending power.

- The strongest uses are frequent and local: grocery top-up, fresh food, fast casual, health, beauty and service categories are easier to defend than car-led destination retail.

Local knowledge and site nuance still matter. When the data view is combined with current operator appetite, local competition, services, parking, loading and fitout requirements, it creates a stronger and more commercially useful pitch.

How We Would Pitch the Site

We would pitch the site as a Bankstown CBD location with three linked strengths: immediate pedestrian/station movement, a large resident market close by, and a substantial pool of customer spending power already moving through the strip. The tenant-facing story is a practical retail opportunity supported by existing movement, local spend depth and frequent everyday missions.

The data points to a clear tenant-facing narrative:

- Convenience and frequency: the site is strongest for everyday categories that benefit from repeat local trips, station access and short-stay missions.

- Market depth: people within a five-minute drive time represent approximately $1.8B of annual retail spend behind the immediate plaza setting.

- Pass-by spending power: customers observed around the site over the past 12 months represent approximately $5.5B of annual spending power across retail, food, service and automotive categories.

- Best-fit categories: specialty grocery, fresh food, fast casual, health, beauty and local services have the strongest fit with the location story.

Key Terms

- Unique customers: estimated unique people observed using the location over the moving annual period. Treat this as an annual customer measure rather than a single-month footfall count.

- Visits: unique day visits observed over the moving annual period. This is closest to a traffic-counter style measure, but based on observed customer movement rather than a door counter.

- 5-minute walk market: residents plus workers in the immediate walkable catchment. Workers are included here because short-walk workday demand is highly relevant to food, service and convenience tenants.

- 5-minute drive market: resident demand within a five-minute drive time. The annual retail spend figure is the yearly retail spend of people in that drive-time market; it is the depth behind the site, but the pitch should still recognise access, parking and pedestrian context.

- Pass-by customer spending power: the annual spending power of the customers observed around the site over the past 12 months, across retail, food, service and automotive categories. Read it as the customer wallet already moving through the strip.

- Sales-equivalent value: observed customer behaviour converted into the annual sales level a comparable retail centre would typically support from that engagement. Use it as a comparative retail-asset benchmark rather than reported tenant turnover.

The sales-equivalent number is useful as a benchmark, but it is more complex than the headline pitch metrics. For this site, current observed customer behaviour translates to approximately $44.2M of sales-equivalent value. That is broadly in line with smaller neighbourhood centres in the national LoculChoices benchmark set, including examples such as Valley Metro (~$44.2M), Thornton Shopping Centre (~$44.2M), Highfields Village Shopping Centre (~$44.1M), and Kingaroy Town Centre (~$44.1M).

The benchmark gives a practical scale reference: the customer movement around the site currently carries a value signal similar to the level of engagement many small neighbourhood centres support. A stronger tenant mix, better activation, or a tenant that gives people more reasons to stop can change the behaviour, increase visitation and lift the value signal over time.

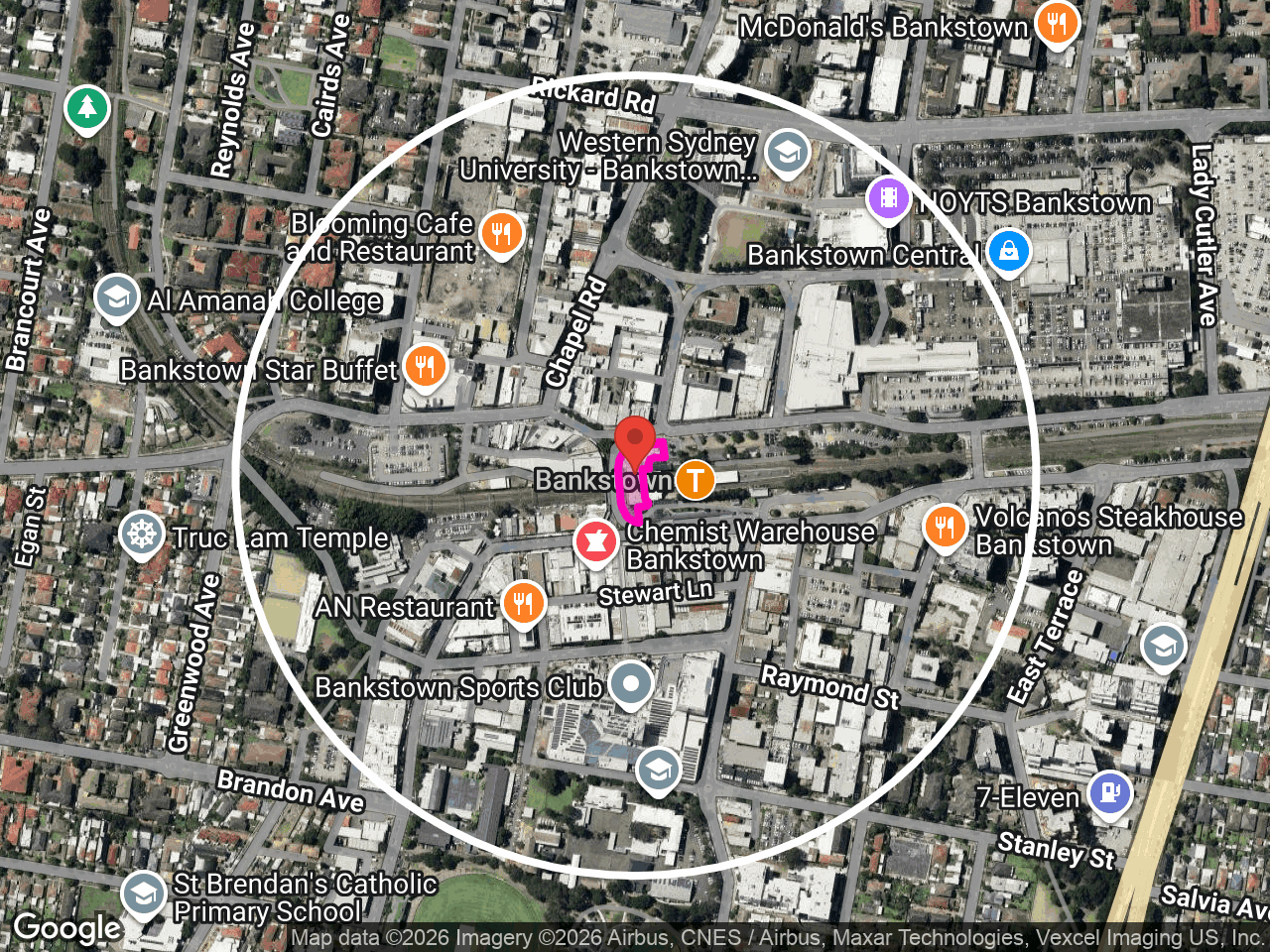

Site Context

The site is best described as a high-exposure Bankstown CBD plaza tenancy with a flexible ground-floor format.

What helps the pitch:

- Subdivision potential materially improves the tenant universe.

- Public parking is nearby, while dedicated customer parking appears limited from the current site evidence.

- Bankstown Station, bus movement, Bankstown Central and the surrounding food/service precinct are all close enough to support a pedestrian-led story.

- The existing premises appear suitable for repositioning, rather than needing to create demand from scratch.

Commercial interpretation:

- A single occupier can work, but only where the operator is comfortable with a plaza/station setting and nearby public parking.

- The cleaner strategy is likely to test subdivision scenarios alongside whole-floorplate users.

- Food can be part of the pitch, subject to services, exhaust, grease trap, loading and council requirements.

- The strongest line is “flexible Bankstown CBD plaza opportunity with measurable local movement behind it.”

Tenant Finder

Tenant Finder combines category demand, brand-location fit, white space, nearby stores and site context, then uses brand benchmarks where available to identify operators worth a leasing conversation. For Bankstown, that matters because the strongest opportunity is not just “fresh food” or “QSR” in general; it is the brands and formats that can use a dense pedestrian plaza, station/worker movement and repeat local errands.

Priority 1 — Fresh food, specialty grocery and daily-needs food

Specialty grocery, Asian grocery, fresh food, produce and butcher/meat are the strongest category themes. Brand-fit examples to test include Harris Farm Markets as a produce benchmark, Tong Li Supermarket for Asian grocery logic, Joe’s Meat Market for butcher/meat, and Lenard’s where poultry/prepared-food format works. These are not automatic lease targets; they are the strongest named examples inside the food-led opportunity.

Priority 2 — Health, nutrition and better everyday food

The health/organic and specialty-grocery layer supports brands such as Go Vita, Nutrition Warehouse, The Source Bulk Foods and Healthy Life. This is useful for a plaza site because the offer can work as a repeat errand, worker-lunch-adjacent or health-led convenience visit rather than relying on a large destination box.

Priority 3 — Compact fast casual, QSR and repeat services

Fast-casual and QSR demand is strong where the format can use station, worker and errand traffic. Brands worth testing include Nando’s, Sushi Train, Roll’d, Sushi Sushi, Subway and Zambrero, subject to tenancy services and fit. Repeat-service examples such as Audika, Barber Industries, Tommy Gun’s and Kingsmen Hair are secondary, but credible if the strategy is subdivision or service-led leasing.

Large showroom/value retail remains possible only for operators comfortable with public parking and a pedestrian plaza setting. The brand list should be used as a targeted outreach and validation list, not as a claim that every named operator will suit the tenancy.

Reachable Market

The reachable-market evidence gives a simple way to describe scale without over-selling the site as a car-led destination.

Useful talking points:

- 5-minute walk: ~3,100 residents and workers, with ~$131M annual retail spend in the walk market.

- 5-minute drive: ~61,000 residents and ~$1.8B annual retail spend within a five-minute drive time.

- 10-minute drive: ~140,000 residents and ~$4.2B annual retail spend within a ten-minute drive time.

- 15-minute drive: ~265,000 residents and ~$8.1B annual retail spend within a fifteen-minute drive time.

- The short-walk catchment is growing at ~4.3% per year over five years, above the national benchmark of ~1.3%.

Commercial implication:

- The site has enough surrounding market depth to support credible tenant conversations.

- The pitch should still start with walk-up, station and repeat local missions, because access and parking shape what operators will believe.

- For prospective tenants, frame this as a “daily routines plus immediate drive-market depth” site.

Addressable Market

Current report month: April 2026.

Headline activity metrics:

- ~195,000 unique customers over the annual period.

- ~1.46M visits over the last 12 months.

- ~4.4 minute average dwell.

- ~$44.2M sales-equivalent value.

How to frame this:

- Read these as annual customer-movement estimates rather than a literal shopfront door counter.

- Sales-equivalent value is a retail benchmarking measure, not reported tenant turnover.

- The total customer figure includes long-tail visitors; it should not be described as the regular weekly shopper base.

- The tighter repeat market is more important for the pitch: the 5-minute drive origin band contributes ~58,000 customers, ~1.23M visits and ~$40.8M sales-equivalent value.

Commercial interpretation:

- Use the headline numbers to show the site is not isolated.

- Use the origin split to keep the story grounded: the opportunity is driven by repeat local movement first, with broader reach adding support.

- The sales-equivalent benchmark helps translate customer behaviour into a retail-performance language prospective tenants understand.

Customer Segments

This view compares two related but different audiences:

- Reachable market: the resident marketing segments within the five-minute drive market.

- Addressable market: the marketing segments actually observed using the site over the annual period.

The two views overlap strongly, which is useful: the neighbourhood types most visible in the local residential market are also the neighbourhood types the site is already attracting. The combined top set produces six segments because the fifth-ranked reachable segment and the fifth-ranked addressable segment are different.

The main customer story is a family and multicultural-suburban story. The strongest groups are concentrated around Yagoona–Birrong, Condell Park, Bankstown South, Bankstown North, Punchbowl, Lakemba, Greenacre South and nearby connected suburbs. They are not one generic “family shopper”: some are value-led family communities, some are established multicultural households, some are new suburban families with very high repeat use, and some are smaller supporting segments that strengthen the everyday convenience case.

1. Value Family Communities

This is the largest segment in both views: around 23.0k people in the five-minute drive market, representing about $696M in annual retail spend, and approximately 65.6k observed customers making 250k visits. They are most visible from Yagoona–Birrong, Condell Park, Punchbowl, Greenacre South and Chester Hill / Sefton.

The pen portrait is practical, family-led and price-aware. These are households managing school routines, grocery budgets, kids’ needs, household basics and quick meals. They will respond to tenants that make everyday life cheaper or easier — value grocery, affordable fresh food, pharmacy, kids’ basics, simple food-to-go, discount household goods and practical services. This group is the anchor audience for the site because it is large locally and already visible in the attracted customer base.

2. Multicultural Suburbs

This is the second-largest reachable and addressable segment: around 16.1k people, $461M in reachable annual spend, and approximately 54.8k observed customers making 360k visits. The strongest customer origins are Bankstown South, Yagoona–Birrong, Bankstown North, Punchbowl and Padstow.

This group is important because it fits the Bankstown CBD context: culturally diverse households, strong local routines, food-led missions and high repeat use. The customer story is a broad local audience with everyday needs across fresh food, specialty grocery, casual dining, services, pharmacy, mobile/repair, banking-style errands and family convenience. Tenant pitches that recognise multicultural food, value, convenience and trusted local service should land better than generic retail positioning.

3. New Suburban Families

This group ranks third in both views: around 14.9k people, $414M in reachable annual spend, and approximately 27.1k observed customers making 613k visits. It is especially strong from Bankstown North, Lakemba, Bankstown South, Yagoona–Birrong and Punchbowl.

The important signal is frequency. This segment has fewer customers than the first two groups, but it generates very high repeat visitation. These are family households using the precinct as part of regular routines — school, work, public transport, food, errands and quick services. For leasing, this is a strong case for daily-needs operators: compact grocery, fresh food, bakery, QSR/fast-casual, pharmacy, beauty, phone repair and practical family services.

4. Community Value Neighbourhoods

This group is fourth in the reachable and observed views: around 2.5k people, $62M in reachable annual spend, and approximately 7.9k observed customers making 40k visits. It draws from Cabramatta / Lansvale, Bankstown North, Yagoona–Birrong, Fairfield East and Bankstown South.

This is a more budget-constrained audience, but it matters because it reinforces the role of the site as practical local infrastructure. These customers are likely to prioritise value, certainty, convenience and essential services. The right operators are those that feel useful and accessible: pharmacy, bulk-billing or allied health, affordable food, discount household goods, service retail, repairs and everyday convenience. The pitch should stay grounded and useful rather than premium-led.

5. Suburban Starters

This is now the fifth-largest reachable segment, with around 1.4k people and $38M in reachable annual spend, and approximately 4.9k observed customers making 74k visits.

The local read is a younger, denser, renter-heavy audience using the precinct for fast, practical routines. They strengthen the case for compact grocery, affordable food-to-go, phone repair, beauty, allied health, pharmacy and everyday services. For leasing, this group is less about premium destination retail and more about convenient formats that work around station access, errands and repeat short trips.

6. Mainstream Suburbia

This segment sits outside the top-five reachable market but is inside the top-five observed audience: around 945 people in the five-minute drive market, $31M in reachable annual spend, and approximately 7.4k observed customers making 8.7k visits. It draws from Bass Hill / Georges Hall, Revesby, Auburn South, Bankstown North and Condell Park.

This is a more classic suburban family audience. It is less frequent than the core Bankstown segments, but it adds useful spend breadth. The customer missions are familiar: grocery, family food, pharmacy, basic apparel, kids’ needs, home errands and service stops. The opportunity is to give these customers a reason to choose the plaza when they are already in the Bankstown CBD, rather than relying on them as the primary repeat base.

The practical read is simple: the site is strongest with value-led family communities, multicultural suburban households and new suburban families. These groups give the tenancy repeat rhythm and daily-use credibility. Supporting starter and mainstream suburban segments add breadth, but the lead positioning should stay focused on everyday convenience, food, family services and practical local missions.

Customer Engagement

The headline engagement story is that the site has retained its visit base while the customer base has become more concentrated. The site recorded approximately 195k customers, down about 10% on last year, while visits were effectively flat at approximately 1.46M. That means the average customer is visiting more often: about 7.5 visits per customer, up from 6.7 last year.

Contact hours are up very strongly year-on-year. That should be read carefully: last year’s dwell/contact-hour base was low, so the growth rate looks especially large. The useful client-facing point is that current customers are now spending more time in and around the location, while visit volume has held steady.

That points to a more concentrated audience. The long tail of casual or low-frequency visitors appears to have thinned, while the core audience is still using the location. For leasing, that matters: a tenant that fits routine daily missions can trade into an audience that is already returning, while the right offer can also rebuild broader casual reach.

The daypart pattern reinforces the same story. Morning activity is up strongly year-on-year, Sunday has improved, and weekday afternoon remains important. The softer areas are evening, lunch and some late-week/weekend periods. So the practical read is: this is a site with resilient routine use, stronger current dwell/contact, and room to improve casual stop-in behaviour.

The leasing implication is practical:

- Lead with the core: the current strength is repeat local demand from residents, workers, station users and people already moving through the plaza/CBD strip.

- Use the frequency story carefully: fewer people are coming through, but the people still coming are using the location more often. That is a better tenant-fit signal than the customer decline looks at first glance.

- Protect and grow the long tail: the right tenant should serve the existing core and give occasional visitors more reasons to stop, especially around evenings, lunch and weekend missions.

- Match the tenant to the rhythm: formats that rely on frequent, short, local missions are more believable than operators that need long dwell, heavy car access or a pure destination-leisure profile.

Cross-Visitation and Precinct Movement

This section looks at where people move on the same day they visit the site. Read it as the activity pattern around the visit itself — roughly the two hours before and after someone is observed around 84–85 Bankstown City Plaza.

The first map shows the journey pattern around the site. Deeper red areas mean higher same-day movement from the same customer journeys. For Bankstown, the pattern is important because activity runs through the plaza, toward Bankstown Central, the station and the surrounding food/service streets. That supports a simple leasing message: the site sits inside an existing CBD movement pattern rather than having to create traffic on its own.

The second map translates that movement into nearby places. It uses mapped building and place outlines — such as shopping centres, larger buildings and other named destinations — to show which places are most strongly connected to the same-day customer journey. This is a relative journey signal rather than a door-counter match. Because people are not observed continuously at every second of the trip, the measure allows for the likelihood of seeing a person within a place during their journey. Read it as a relative strength signal: which nearby places are most likely to be part of the same customer mission.

Useful framing:

- Customers are already moving between the plaza, station, Bankstown Central and surrounding food/service uses.

- The opportunity is to place the right operator into an existing daily movement pattern.

- The tenancy can intercept known movement if the tenant format is right.

- The strongest tenant story is about convenience, routine and passing missions across the surrounding CBD/plaza movement pattern.

This section is most useful when paired with current market knowledge: nearby operators, vacancies, incentives, rents, fitout expectations and current expansion appetite.

Category and Tenant Pitch Plays

1. Asian / Specialty Grocery

Best use: medium-format or subdivided grocery/specialty food operators.

Why it is worth a conversation:

- Strong local food and grocery demand.

- Dense Bankstown catchment with frequent daily-needs missions.

- Plaza/station context suits top-up trips and walk-up trade.

Pitch language:

- “The data supports a strong local grocery and specialty-food story. The best fit will be an operator that can trade from pedestrian movement, station access and nearby public parking.”

Watch-outs:

- Do not pitch Tong Li as clean white space without further validation; public search indicates existing Bankstown presence.

- Prioritise independent, regional or format-flexible Asian grocery, pantry, deli and fresh-food operators.

2. Fresh Food / Butcher / Produce

Best use: smaller fresh-food specialists, not large car-dependent fresh markets.

Why it is worth a conversation:

- Greengrocer/produce, butcher/meat and specialty grocery score strongly at category level.

- The site has repeat local movement and strong daily-needs spend.

- Subdivision could create a more believable fresh-food tenancy than one oversized operator.

Pitch language:

- “The demand signal is strong for fresh food, but the right operator needs to match a Bankstown CBD plaza format.”

Watch-outs:

- Treat Harris Farm as a category signal. A direct recommendation needs parking, loading and format proof.

- Better targets may be local produce, butcher, deli, seafood or specialty operators that can trade from walk-up movement.

3. Fast-Casual / QSR

Best use: subdivided frontage, food-to-go or compact dine-in.

Why it is worth a conversation:

- Fast-casual and QSR show very strong demand signals.

- Weekday morning and afternoon activity supports station, worker and errand behaviour.

- Smaller food formats can work better than car-led formats.

Potential brand leads to validate:

- Guzman y Gomez — strong brand signal; existing Bankstown Airport store means the CBD/plaza gap needs validation.

- Grill’d — good context fit if store-size and nearby competition work.

- Schnitz — possible station/centre format if services and fitout are feasible.

- Zambrero — strong demand signal; validate current local absence and tenancy requirements.

- Sushi Sushi / Roll’d — smaller centre-style formats may fit a subdivided shop, subject to local competition.

Watch-outs:

- Lead with compact food formats that match station, worker and errand movement.

- Check services early: exhaust, grease trap, loading, waste and approvals.

4. Health, Beauty and Local Services

Best use: smaller subdivided tenancies.

Why it is worth a conversation:

- The precinct already supports repeat service behaviour.

- These tenants can benefit from transport access and daily pedestrian exposure.

- They do not need the full tenancy, which makes them useful in a subdivision strategy.

Potential directions:

- Barber / men’s grooming.

- Beauty / skin / wellness.

- Allied health, hearing and appointment-led services after local-store validation.

- Supplements / wellness only where the immediate market is not already well served.

Pitch language:

- “Bankstown City Plaza can support smaller service tenants that want exposure, access and repeat local missions without taking a shopping-centre style footprint.”

5. Large Showroom / Value Retail

Best use: only where the operator is comfortable with public parking and a pedestrian CBD setting.

Why it may still be relevant:

- The existing premises already read as a large showroom shell.

- The floorplate can suit display-led retail where car dependency is manageable.

Watch-outs:

- Limited dedicated parking weakens bulky, heavy-goods and destination-showroom pitches.

- Treat this as a selective conversation, not the lead story.

Suggested Positioning

If one clean narrative is needed, use this:

- Lead message: “A flexible Bankstown CBD plaza tenancy with station-led movement, immediate local spend depth and subdivision upside.”

- Best-fit tenant groups: specialty grocery/fresh food, compact fast-casual/QSR, health/beauty/services and selected showroom/value operators.

- Proof points: subdivision potential; ~3,100 short-walk resident/worker market; ~61,000 5-minute drive resident market; ~$1.8B annual retail spend within a five-minute drive time; ~1.46M annual visits; ~$5.5B pass-by customer spending power; weekday-led engagement.

- Commercial judgement required: validate operator presence, services, loading, parking expectations, tenancy split, incentives and current expansion appetite.

The right final pitch should feel confident: the data shows a strong local opportunity, and the site-specific commercial layer determines which operators are most likely to convert.

References and Source Notes

Use the site-context material with source notes. The traffic counts are vehicle counts, not pedestrian counts, and should not be blended into the customer / visit analysis.

Site listing / physical context

- W.T. Newey & Co. listing: “84–85 Bankstown City Plaza, Bankstown NSW 2200.” Source for ground-floor retail/showroom context, subdivision potential, public car parks nearby, heavy foot traffic, metres from Bankstown Train Station and moments from Bankstown Central. URL: https://www.neweystrata.com.au/listing/l40070544-shop-2-84-85-bankstown-city-plaza-bankstown-nsw-2200/

Transport and road-movement references

- TfNSW Open Data — Train, Metro and Light Rail Station Entries and Exits. Used for Bankstown Station entry/exit sanity check. Current CSV resource: https://opendata.transport.nsw.gov.au/data/dataset/3977df59-a1fa-422e-91ff-cfaeac355cc9/resource/f8bb2918-0540-4bb3-9ccf-f7aef04d4249/download/entry_exit.csv

- TfNSW Open Data — NSW Roads Traffic Volume Counts API / generated CSVs. Used for nearby road vehicle-count context. Dataset page: https://opendata.transport.nsw.gov.au/data/dataset/nsw-roads-traffic-volume-counts-api

- Nearby vehicle-count examples from TfNSW yearly summary / station-reference CSVs: Fairford Road south of Aster Avenue ~30.8k vehicles/day (2022, ~1.0 km); Stacey Street east of Frederick Street ~55.5k (2009, ~1.3 km); Hume Highway east of Stacey Street ~60.8k (2022, ~1.6 km); Canterbury Road west of Stacey Street ~57.9k (2018, ~1.8 km). TfNSW notes traffic-volume data-quality and sensor-availability issues, so present these as directional road-exposure references only.